Global LNG demand is increasing

Source: METI, LNG Producer-Consumer Conference, June 2025

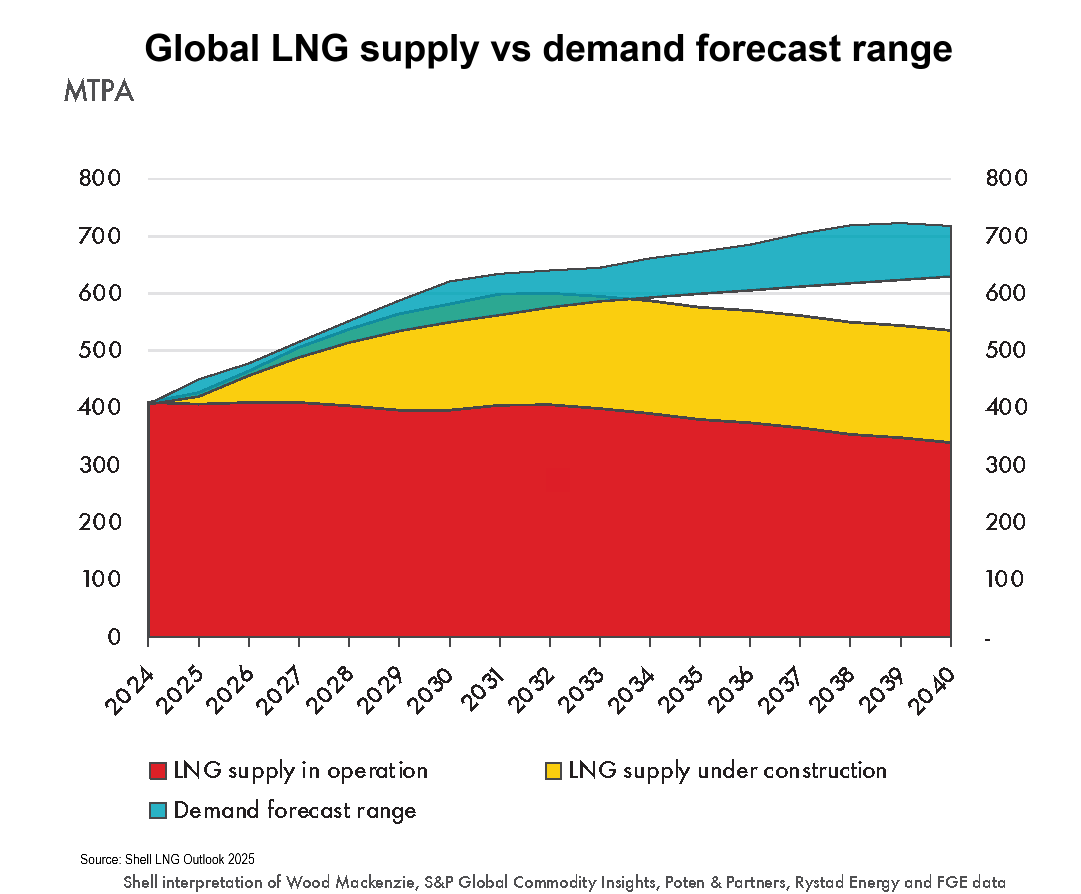

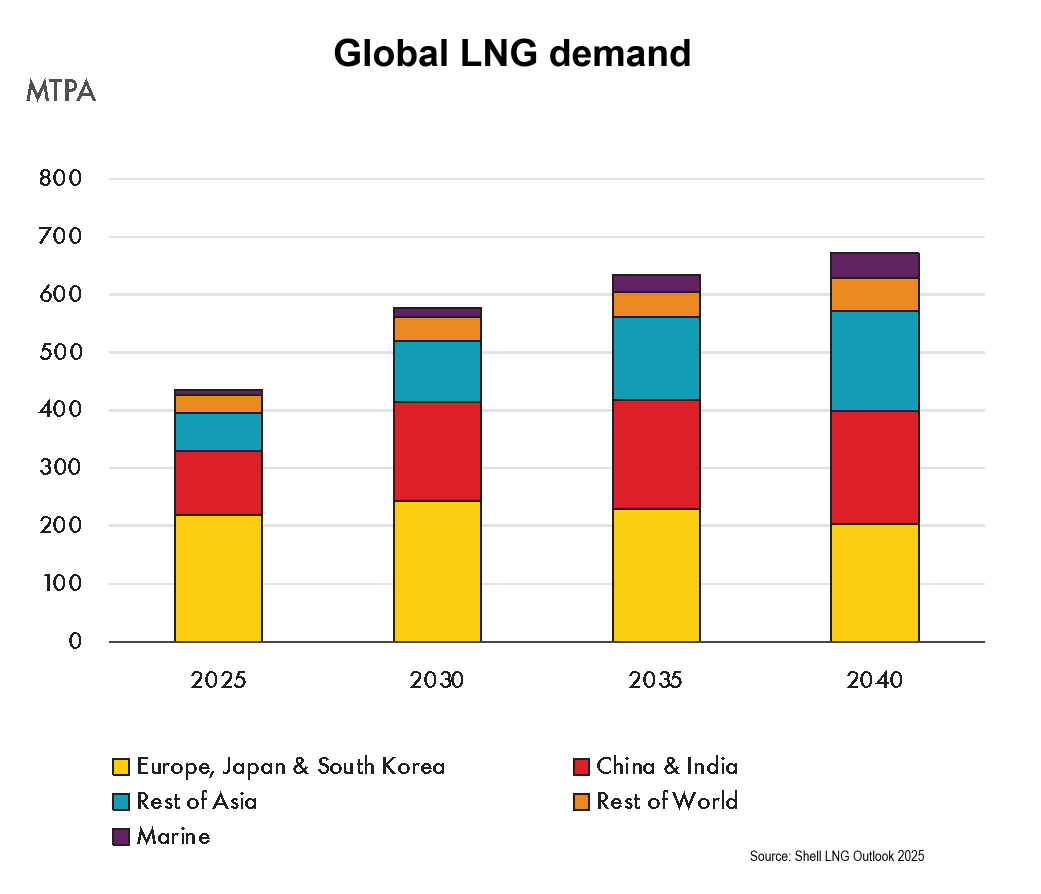

Shell’s LNG Outlook 2025 forecasts demand for liquefied natural gas (LNG) will rise by around 60% by 2040 (refer to chart above, left), largely driven by economic growth in Asia, emissions reductions in heavy industry and transport as well as the impact of artificial intelligence. Industry forecasts now expect LNG demand to reach 630-718 million tonnes a year by 2040, a higher forecast than last year. More than 170 million tonnes of new LNG supply is set to be available by 2030, helping to meet stronger gas demand, especially in Asia, but start-up timings of new LNG projects are uncertain. Shell also expect a continuing global LNG supply shortfall from about 2034.

“Upgraded forecasts show that the world will need more gas for power generation, heating and cooling, industry and transport to meet development and decarbonisation goals,” says Tom Summers, Senior Vice President for Shell LNG Marketing and Trading. “LNG will continue to be a fuel of choice because it’s a reliable, flexible and adaptable way to meet growing global energy demand.”

China is significantly increasing its LNG import capacity and aims to add piped gas connections for 150 million people by 2030 to meet increasing demand. India is also moving ahead with building natural gas infrastructure and adding gas connections to 30 million people over the next five years.

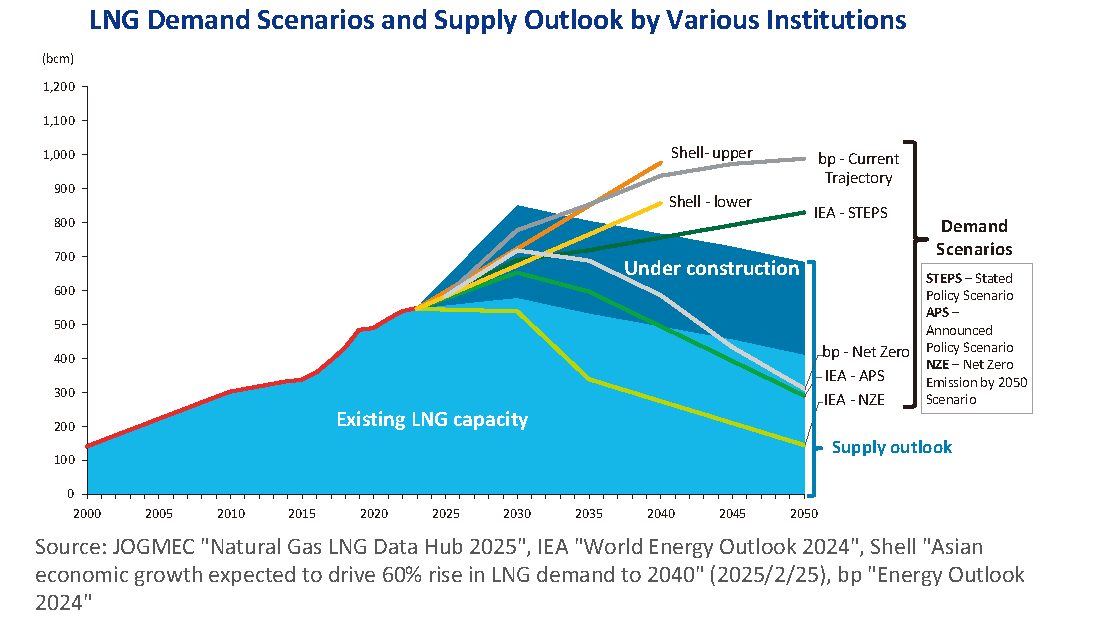

At the 2025 LNG Producer-Consumer Conference the Japanese Ministry of Economy, Trade and Industry (METI) stated LNG supply is expected to broadly align with demand scenarios projected by various institutions through the early 2030s. However, under high-demand scenarios, supply could become tight in the latter half of the 2030s (refer to chart above, right). On the supply side, projections are subject to significant uncertainty in the energy market, with the realization of planned and future LNG projects dependent on investment profitability and access to financing. On the demand side, particularly in emerging economies across Asia, it is important to recognize that demand levels may fluctuate depending on gas price trends, as these economies continue to grow. Under various Net-Zero scenarios an LNG surplus is forecast, but current evidence strongly suggests that the world will fall well short of Net-Zero by 2050, given the huge investments required and the potentially negative economic consequences on the way to getting there.

In the METI’s view, economic growth is expected to drive a continued increase in energy demand, and natural gas, including LNG, is anticipated to play an important role in meeting this growth. Gas-fired power plants contribute to power system stability by balancing the intermittency associated with the expansion of renewable energy. Additionally, as gas-fired generation emits fewer greenhouse gases than coal, fuel switching can support emissions reductions. Moreover, existing gas and LNG infrastructure can be repurposed for emerging low-carbon fuels such as biogas, e-methane, hydrogen, and ammonia, offering further decarbonization potential across the energy value chain. As such, LNG is expected to retain an important role during the energy transition.

Investment in upstream natural gas assets declined between 2015 and around 2020. This was due to a combination of factors, including the oil price decrease, policy and demand uncertainty following the Paris Agreement, increasingly stringent regulations on upstream oil and gas investments, and a strategic shift among energy companies toward renewables. Additionally, energy companies with high leverage suffered from the sharp decline in oil prices. However, since 2021, heightened concerns over energy security, particularly following Russia’s invasion of Ukraine, and the associated spike in commodity prices have reignited upstream investment. Investment in LNG liquefaction projects, which had been constrained during the oil price slump, surged in 2018–2019 in anticipation of the increase of oil price and demand recovery. In 2019, the volume of liquefaction capacity reaching final investment decision (FID) marked a record high. Since 2021, large-scale projects such as Rio Grande Phase 1, Port Arthur Phase 1, and Plaquemines Phase 2 in the United States, and the North Field expansion in Qatar, have also reached FID, pushing liquefaction investment volumes upward.

Remarkably, Australia has not played a major role in this LNG investment surge.

Natural gas is essential for the global energy transition, as evidenced by growing LNG demand

Since the outbreak of the conflict in Ukraine, European and Asian countries more than most have recognized that they must reduce reliance on any one region or country’s supply of energy including natural gas.

Natural gas is both a transition and a destination fuel. Natural gas and LNG are essential for the energy transition as they play an instrumental role in shifting away from coal and moving toward net-zero emissions. As the transition evolves, natural gas will remain vital in providing reliable and efficient energy to support economies in different parts of the world including Australia and all of Asia.

The re-drawing of global energy supply maps is pushing natural gas and LNG demand to new heights and spurring new off-take contracting and other activities and opportunities for companies like Gulf Energy, for example:

Delfin Midstream said on Wednesday it has taken a positive final investment decision for the first floating liquefied natural gas (FLNG) vessel of the Delfin LNG project under development offshore Louisiana in the Gulf of Mexico. Delfin FLNG 1 will be the first floating liquefaction facility in the U.S. and the largest FLNG project globally, with an expected export capacity of 4.4 million tonnes of LNG per year.

Liquefied natural gas deliveries to China are showing signs of recovery, as some buyers replace shipments disrupted by the conflict in the Middle East. The 30-day moving average for LNG imports has increased to the highest level since late February, according to ship-tracking data compiled by Bloomberg. Although that's still below the five-year average, the gap has shrunk to roughly half of what it was in early April. (Rigzone, 12 May 2026)

Pakistan opted not to buy urgent cargoes of liquefied natural gas on the spot market, betting that hostilities which have closed the Strait of Hormuz will ease and cheaper supplies from Qatar will arrive soon. (Rigzone, 8 May 2026)

Cheniere Energy (LNG) settled down 5.6% Thursday to its lowest in nearly two months after posting a $3.5B Q1 loss driven by billions of dollars in losses tied to derivative contracts, as the Middle East war upended energy markets. (MSN, 8 May 2026)

Abu Dhabi National Oil Co. has managed to keep a trickle of liquefied natural gas exports moving through the Strait of Hormuz by concealing tanker locations, as established producers shift tactics to navigate the conflict. (Rigzone, 7 May 2026)

Russia's exports of liquefied natural gas rose 8.6% in January to April to 11.4 million metric tons from the same period last year due to supplies from the Arctic LNG 2 project, which reached 1 million tons in the first four months of the year, preliminary LSEG data showed on Tuesday. (Reuters, 5 May 2026)

Camuzzi Gas Inversora and Vitol signed a Memorandum of Understanding (MoU) in connection with development of the LNG del Plata project. Vitol could purchase up to 100% of production and will evaluate an equity stake in the project. (Oil & Gas Journal, 5 May 2026)

State producer QatarEnergy extended force majeure on its liquefied natural gas supply through mid-June, according to people familiar with the matter, as the Strait of Hormuz remains almost entirely closed to tanker traffic. (Rigzone, 4 May 2026)

Australia’s Woodside Energy is having trouble finding buyers for the liquefied natural gas it produces at its Louisiana LNG plant, Reuters has reported, citing unnamed sources. The reason is that Woodside is asking for higher liquefaction fees than other LNG exporters in the United States. (OilPrice.com, 1 May 2026)

Petroliam Nasional Bhd (Petronas) has signed a deal to give returning investor ENEOS Group a 10 percent ownership in Malaysia LNG (MLNG) Tiga Sdn Bhd. The agreement gives the Japanese energy company a 10-year stake in the facility in Sarawak state, after ENEOS' previous participation expired 2023. ENEOS' operated SK-10 Block is among offshore reservoirs supplying feed gas to the liquefaction project. (Rigzone, 1 May 2026)

Woodside Energy Group Ltd said Wednesday its liquefied natural gas (LNG) shipments have not been impacted by the conflict in the Middle East and that it has largely avoided increased costs from higher carrier rates. (Rigzone, 29 April 2026)

China’s imports of liquefied natural gas this month are expected to be the lowest since 2018, based on data from Kpler, Bloomberg has reported, citing soaring prices. April LNG arrivals are seen at 3.5 million tons, which would also be a 30% drop on a year ago, the report said. An earlier report by Reuters pegged China’s LNG imports for April at 3.36 million tons, again based on Kpler figures, comparing that to a total 7.66 million tons for December, during the seasonal demand peak. (OilPrice.com, 29 April 2026)

French major TotalEnergies posted a $5.4bn net income in Q1, bolstered by a 12% jump in liquefied natural gas (LNG) production and trading activities during the current market volatility. (GasWold, 29 April 2026)

The United States and U.S. companies signed deals worth billions of dollars with Balkan countries on Tuesday, boosting Washington's energy presence in the region and backing AI development. (Reuters, 29 April 2026)

The first LNG vessel to cross the Strait of Hormuz since the end of February has exited the chokepoint and is currently nearing India’s shores, Bloomberg reported, citing tanker-tracking data. (OilPrice.com, 28 April 2026)

Facebook's parent company said Monday it has signed up for potential capacity from a project to harvest solar power in space and another project to enable "ultra-long-duration" battery energy storage. (Rigzone, 28 April 2026)

Shipyards are expected to deliver up to 100 new LNG carriers this year, up from 79 last year, as new projects in the U.S. and demand for new and more efficient vessels to replace retiring carriers drive increased orders despite the uncertainties stemming from the Middle East war. A record high number of 90-100 liquefied natural gas carriers (LNGC) are set to be delivered in 2026, according to estimates by analysts at Poten & Partners and Drewry, Reuters reports. (OilPrice.com, 27 April 2026)

LNG carriers impacted by the Middle East war are expected to be the last to return to normal due to extremely high insurance risks and low risk tolerance for high-value cargoes. (GasWorld, 27 April 2026)

Japan's biggest LNG importer and largest power producer, JERA, has secured its LNG supply through July and will adjust its procurement strategy to be more flexible amid the Middle East conflict that has trapped LNG supply behind the Strait of Hormuz. (OilPrice.com, 27 April 2026)

Shell is doubling down on North American gas in a major bet on long-term LNG demand, agreeing to buy Canada’s ARC Resources in a $16.4-billion deal that will add roughly 370,000 barrels of oil equivalent per day to production and strengthen the supermajor’s position in one of the continent’s most strategic gas corridors. (OilPrice.com, 27 April 2026)

Global orders to build liquefied natural gas carriers (LNGC) are set to rebound this year after a 2025 slump as growing LNG output and vessel fuel efficiency drive demand, industry executives and analysts say. (Reuters, 27 April 2026)

Rio Grande LNG has requested an extension from the Federal Energy Regulatory Commission (FERC) to complete construction of its liquefied natural gas export terminal in Texas, according to an April 24 filing. (Pipeline & Gas Journal, 27 April 2026)

The Government of Canada has unveiled a $25-billion sovereign investment vehicle aimed at accelerating large-scale energy and infrastructure projects, signaling increased federal support for oil, gas and LNG development. (WorldOil.com, 27 April 2026)

U.S. Department of the Interior has reached agreements with two offshore wind developers to terminate lease positions and redirect capital into conventional energy projects, marking a notable shift in U.S. energy policy and investment flows. (WorldOil, 27 April 2026)

Record-high U.S. LNG exports have managed to mitigate so far the shock supply loss from Qatar, but American exporters are unlikely to continue running facilities at full capacity for all of this year as maintenance and hurricane season are likely to curtail some supply in the coming months. (OilPrice.com, 27 April 2026)

Europe is beginning the roll-out of a ban on imports of Russian liquefied natural gas at a difficult time, with the war in Iran seriously disrupting global supply. From Saturday, the European Union will prohibit purchases of Russian LNG on a short-term basis, known as the spot market. Supplies under long-term contracts can continue until the end of the year, but the ban could still create challenges. (Rigzone, 25 April 2026)

U.S. LNG exporters have so far offset the drop in shipments from Qatar following Iranian attacks on its facilities and the closure of key Middle East shipping lanes, ensuring that total supplies remain at record highs despite the war. (Reuters, 24 April 2026)

Pakistan is tapping the spot LNG market for the first time in nearly three years as the lack of fixed-term Qatari supply has triggered a power crisis and widespread outages. (OilPrice.com, 24 April 2026)

Golden Pass LNG, designed to export about 18 million metric tons per annum (MMtpa), has dispatched its inaugural cargo. (Rigzone, 23 April 2026)

Pakistan has been at the center of media coverage of the Middle East war as the country that took up the initiative to moderate peace talks. It also happens to be the country arguably most hurt by the war without being directly involved in the hostilities. (OilPrice.com, 21 April 2026)

An LNG tanker has arrived at the Golden Pass facility in Texas to collect the plant's inaugural export of the superchilled gas, the company confirmed on Monday, after finally beginning production earlier this year following prolonged delays in construction. (Reuters, 21 April 2026)

Thanks to the more than $300 million services contract to Green Tug Towing, a joint venture of Harbor Docking & Towing and Saltchuk Marine, for the design and construction of four new tugs to be built at C&C Marine and Repair in Belle Chase and delivered to Louisiana LNG in 2028, Woodside and its contractors have now committed more than $1 billion to Louisiana suppliers for the foundational development of this LNG project. (Offshore Energy, 20 April 2026)

The U.S.-flagged American Energy LNG carrier has reached one year of uninterrupted operations in March 2026, delivering 2 million cubic meters (approximately 549 million gallons) of U.S.-sourced LNG to Puerto Rico, enough to power about 1.2 million homes annually and reduce emissions by nearly 30% compared to diesel. (Offshore Energy, 17 April 2026)

Exxon has withdrawn offers to sell initial LNG cargoes from the Golden Pass export project as the facility operates below capacity during startup. The plant, a joint venture with QatarEnergy, is still ramping up production following delays and cost overruns. (Pipeline & Gas Journal, 17 April 2026)

Venture Global Inc said its subsidiary overseeing the Calcasieu Pass LNG project in Cameron Parish, Louisiana has entered into a $1.75 billion credit facility. (Rigzone, 17 April 2026)

The US-Israeli war on Iran has been hugely damaging for Iran and for its noncombatant Gulf neighbors, which have suffered both widespread attacks and an inability to export oil and gas at customary levels. A country-by-country assessment shows these damaging effects are unevenly spread, with one or two countries seeing windfall revenues while others undergo devastating losses. (Oil & Gas Journal, 16 April 2026)

In a market update sent to Rigzone on Wednesday, Rystad Energy noted that its analysis shows that repair and restoration costs for energy-linked infrastructure, as a result of war in the Middle East, could hit $58 billion. (Rigzone, 16 April 2026)

NextDecade Corp.’s Rio Grande LNG LLC has awarded Honeywell International Inc. a contract to supply liquefaction process technology and equipment for Trains 4 and Train 5 of its 30-million tonne/year (tpy) plant, under development in Brownsville, Tex. The award was made through an agreement with engineering, procurement, and construction contractor Bechtel Energy Inc. (Oil & Gas Journal, 16 April 2026)

The United States is in the midst of a historic expansion of its liquefied natural gas (LNG) export infrastructure. After a decade of rapid growth that transformed the U.S. from a minor player into the world’s largest LNG exporter, a new wave of projects under construction and recently sanctioned is poised to add more than 6 Bcf/d of incremental export capacity in the near term—primarily by the end of 2026—with even larger additions planned through 2029. This buildout, concentrated along the Gulf Coast, is supported by abundant domestic natural gas supply, strong global demand, and favorable policy tailwinds. (Energy News Beat, 16 April 2026)

Colombian power plants are preparing to ramp up liquefied natural gas imports ahead of an expected El Niño, which would bring dry weather to the Andean country. (Rigzone, 15 April 2026)

According to International Energy Agency Executive Director Fatih Birol, there is a “disconnect” between how markets are perceiving the energy crisis and the reality on the ground in the Middle East. (Atlantic Council, 14 April 2026)

On Mar. 26, 2026, Commonwealth LNG LLC agreed to sell Glencore Ltd. an additional 1 million tonnes/year (tpy) of LNG for a term of 20 years from its planned 9.5-million tpy plant in Cameron Parish, La. The two companies had reached a 2-million tpy, 20-year agreement in March 2025. (Oil & Gas Journal, 14 April 2026)

Iran said it would target all ports in and close to the Persian Gulf if its own shipping hubs are threatened, heightening the standoff over the Strait of Hormuz after the US announced plans for a blockade of Tehran-linked vessels. (Rigzone, 13 April 2026)

The global LNG supply-demand balance is unlikely to be substantially altered by the announcement of a two-week ceasefire between the US and Iran, because of expected continued uncertainty over shipping insurance, security and production facilities. Just under 1.2mn t of LNG across 15 carriers remains trapped west of the strait of Hormuz, data from vessel tracker Kpler show. One vessel, the 155,000m³ Gaslog Skagen, has delivered to Kuwait's 24mn t/yr Al Zour LNG import terminal three times since the war in the Middle East began, and is charting a course for Al Zour at present. (Argus Media, 9 April 2026)

See past activities and opportunities for companies like Gulf Energy below:

Future global LNG demand will come mainly from Asia, and the Bamaga Basin (Q/23P) is ideally located to supply that market

Australia is ‘location competitive’ for much of Asia

Asia’s demand for LNG is forecast to surge, but Australia hasn’t found and developed enough new gas to remain a major global LNG supplier

Australia is closer to most high potential Asian markets than its biggest LNG exporting competitors, Qatar and the USA.

Australia has failed to maintain a steady stream of new gas production projects being brought online.

More than $200 billion of LNG projects were approved for final investment decisions (FIDs) in Australia before 2012. Since then, the Woodside Scarborough Project (Pluto Train 2 Expansion) and the Santos Barossa Project are the only LNG projects to reach FID, with the latter being primarily a backfill project to extend the life of the Darwin LNG facility.

Without further investment in new LNG trains and upstream infrastructure, Australia will lose its position as a major LNG exporter and will almost certainly lose its energy security.